| << Chapter < Page | Chapter >> Page > |

A rise in income causes the budget constraint to shift to the right. In graphical terms, the new budget constraint will now be tangent to a higher indifference curve, representing a higher level of utility. A reduction in income will cause the budget constraint to shift to the left, which will cause it to be tangent to a lower indifference curve, representing a reduced level of utility. If income rises by, for example, 50%, exactly how much will a person alter consumption of books and doughnuts? Will consumption of both goods rise by 50%? Or will the quantity of one good rise substantially, while the quantity of the other good rises only a little, or even declines?

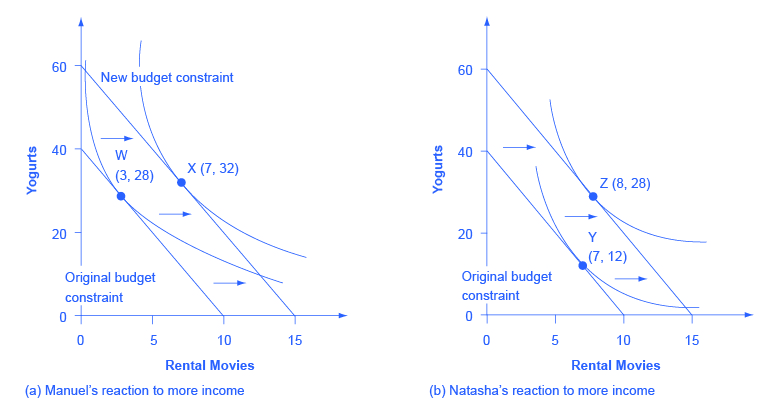

Since personal preferences and the shape of indifference curves are different for each individual, the response to changes in income will be different, too. For example, consider the preferences of Manuel and Natasha in [link] (a) and [link] (b). They each start with an identical income of $40, which they spend on yogurts that cost $1 and rental movies that cost $4. Thus, they face identical budget constraints. However, based on Manuel’s preferences, as revealed by his indifference curves, his utility-maximizing choice on the original budget set occurs where his opportunity set is tangent to the highest possible indifference curve at W, with three movies and 28 yogurts, while Natasha’s utility-maximizing choice on the original budget set at Y will be seven movies and 12 yogurts.

Now, say that income rises to $60 for both Manuel and Natasha, so their budget constraints shift to the right. As shown in [link] (a), Manuel’s new utility maximizing choice at X will be seven movies and 32 yogurts—that is, Manuel will choose to spend most of the extra income on movies. Natasha’s new utility maximizing choice at Z will be eight movies and 28 yogurts—that is, she will choose to spend most of the extra income on yogurt. In this way, the indifference curve approach allows for a range of possible responses. However, if both goods are normal goods, then the typical response to a higher level of income will be to purchase more of them—although exactly how much more is a matter of personal preference. If one of the goods is an inferior good, the response to a higher level of income will be to purchase less of it.

A higher price for a good will cause the budget constraint to shift to the left, so that it is tangent to a lower indifference curve representing a reduced level of utility. Conversely, a lower price for a good will cause the opportunity set to shift to the right, so that it is tangent to a higher indifference curve representing an increased level of utility. Exactly how much a change in price will lead to the quantity demanded of each good will depend on personal preferences.

Notification Switch

Would you like to follow the 'Openstax microeconomics in ten weeks' conversation and receive update notifications?

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|