For the moment we will assume that Equations (2) and (3) are true representations of the world. What then can we do to estimate (2)? What we need to do is find a way to transform (2) so that the error term of whatever regression we estimate does not exhibit autocorrelation. In time period

we have:

Multiply (4) by

to get:

Now subtracting (5) from (4) gives:

or, equivalently,

Let

and

Remember that (3) implies that

Thus, we have:

where

Thus, we have a regression for which the OLS estimates will be BLUE (Best Linear Unbiased Estimator) if we only knew the true value of

Cochran and Orcutt [1949] use this algebra to suggest one way to estimate (6). The estimation entails several steps. First, you use OLS to estimate (2). Second, you estimate (3) using the residuals from the first stage to approximate

This regression gives an estimate of

In the third step, you use the estimate of

to construct estimates of

and

In the fourth step, you use the estimates of

and

to estimate (6); this will yield new estimates of

and

. You then repeat step (2) using these new estimates of

and

to calculate the residuals and then repeat with steps (3) and (4). You continue the process until the estimate of

does not change anymore (i.e., until the change in the estimate of

is less than some value chosen by the researcher). There are a multitude of alternative ways of estimating

[See Greene (1990): Chapter 15 for a full discussion of these methods.] Once you have an estimator for

there exist two major ways of completing the estimation—the Cochran-Orcutt procedure described above and the Prais-Winsten (1954) estimator. The latter estimation procedure does not involve dropping the first observation (as does the Cochran-Orcutt) estimator. In large samples these two estimation techniques are likely to be very similar. In small samples the two techniques may produce estimates that are substantially different.

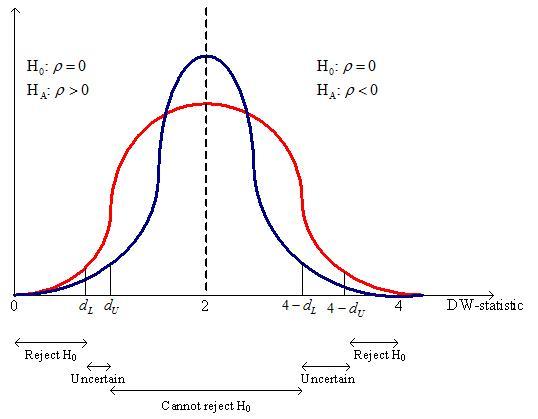

We now turn to the issue of detecting the existence of autocorrelation. In what follows we focus mainly on the detection of first-order autocorrelation as shown in Equation (3). We can use the Durbin-Watson test to see if our suspicions are correct. The Durbin-Watson statistic tests the hypothesis:

Limiting distributions for the Durbin-Watson statistic.

The details of the test statistic can be found in any econometrics textbook and need not detain us here. What you need to know about the DW-statistic are (1) it has a mean value of 2; (2) because its distribution lies between two limiting distributions, we need to look at two critical values. For this reason there are two critical values—one for each of the limiting distributions. Figure 3 illustrates the probability distribution function (pdf) for the Durbin-Watson statistic. The true pdf lies somewhere between the blue pdf and the red pdf. What is shown in the figure is the point below which, say, 5 percent of the distribution lies for each distribution. The true critical point lies somewhere between

and

These values are relevant to testing the null hypothesis of no autocorrelation against the alternative hypothesis of positive autocorrelation

the transfer of energy by a force that causes an object to be displaced; the product of the component of the force in the direction of the displacement and the magnitude of the displacement

A wave is described by the function D(x,t)=(1.6cm) sin[(1.2cm^-1(x+6.8cm/st] what are:a.Amplitude b. wavelength c. wave number d. frequency e. period f. velocity of speed.

A body is projected upward at an angle 45° 18minutes with the horizontal with an initial speed of 40km per second. In hoe many seconds will the body reach the ground then how far from the point of projection will it strike. At what angle will the horizontal will strike

Suppose hydrogen and oxygen are diffusing through air. A small amount of each is released simultaneously. How much time passes before the hydrogen is 1.00 s ahead of the oxygen? Such differences in arrival times are used as an analytical tool in gas chromatography.

the science concerned with describing the interactions of energy, matter, space, and time; it is especially interested in what fundamental mechanisms underlie every phenomenon