| << Chapter < Page | Chapter >> Page > |

Now, in the example if real GDP per hour of labor falls below the $20 subsistence level ($20 per hour of labor), population falls . If real GDP per hour of labor rises above $20, the population rises .

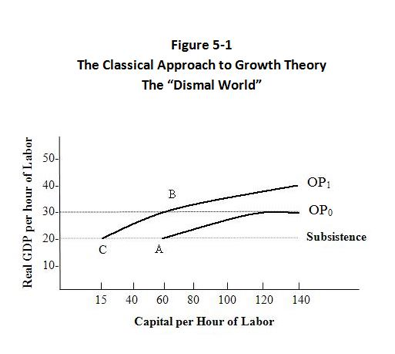

In figure 5-1, the, economy begins at point A with real GDP/hour at $20 and the amount of capital per hour of labor at $60.

At this point, it is important to note that the outcome of the Classical Theory depends on diminishing returns to capital, i.e. the more labor applied to a fixed amount of capital must mean → successfully smaller increments to output. Also, in classical theory, all capital is just Physical capital. No Knowledge capital, no Human capital, no intangible capital.

Source Needed:_____________

(Parkin book – Lookup)

To illustrate classical growth theory, we begin with an original productivity curve OP 0 - showing how real GDP/hour changes as the amount of capital per labor hour changes, given the state of technology.

So, with given technology and productivity curve OP0 the economy is at point “A” (subsistence).

Consider now what happens if there is a technological advance? (Steam engines, cotton gin, etc.). This yields a new productivity curve OP1 and higher productivity per labor hour.

Now, economy moves to point “B.” But, here real GDP hour exceeds subsistence. Result- population grows, as in the Malthus construct.

With more labor being applied to constant capital per hour, real GDP/hour falls back to $20. At point C, because of Law of Diminishing Returns. GDP/hour drops back to subsistence level. You can do no better. Forget about bettering the human condition. Of course, the classical theory is now seen as only a highly deficient explanation of growth before 1820.

Economists views of determinants of growth have, thankfully, changed greatly in the last century.

Growth theory of the 20 th and 21 st century holds that real GDP/hour can grow and that growth can persist for long periods. The human condition can be improved.

As we shall see, Newer Growth Theories hold that pursuit of economic incentives (profit) and innovation can lead to sustained growth. In the New Growth Theory, Human Capital (Knowledge capital), becomes important.

Knowledge of course, is a form of capital that is not subject to law of diminishing returns. (If I use knowledge on the internet, is there any less for available for you)?

Recall, diminishing returns in production arises when one resource is fixed (say capital), and the amount of another resource is unchanged .

But , we now recognize that an innovation and expansion in the stock of knowledge makes both labor and Physical capital (machines) more productive. So, an increase in knowledge capital does not bring diminishing returns.

Growth and Development are complex processes. One way we try to come to grips with this complexity is to build models. Model building is very important and valuable in our efforts to understand the growth process. It is important not to fall into the trap of believing that what was once good for now wealthy countries in 19th and 20th centuries is always good for poorer nations in the 21st century. For one thing there are vast differences in initial conditions that faced now rich nations and the initial condition facing most developing nation.

Notification Switch

Would you like to follow the 'Economic development for the 21st century' conversation and receive update notifications?

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|