| << Chapter < Page | Chapter >> Page > |

The second development regulates federal grants, that is, transfers of federal money to state and local governments. These transfers, which do not have to be repaid, are designed to support the activities of the recipient governments, but also to encourage them to pursue federal policy objectives they might not otherwise adopt. The expansion of the federal government’s spending power has enabled it to transfer more grant money to lower government levels, which has accounted for an increasing share of their total revenue.

See Robert Jay Dilger, “Federal Grants to State and Local Governments: A Historical Perspective on Contemporary Issues,”

Congressional Research Service , Report 7-5700, 5 March 2015.

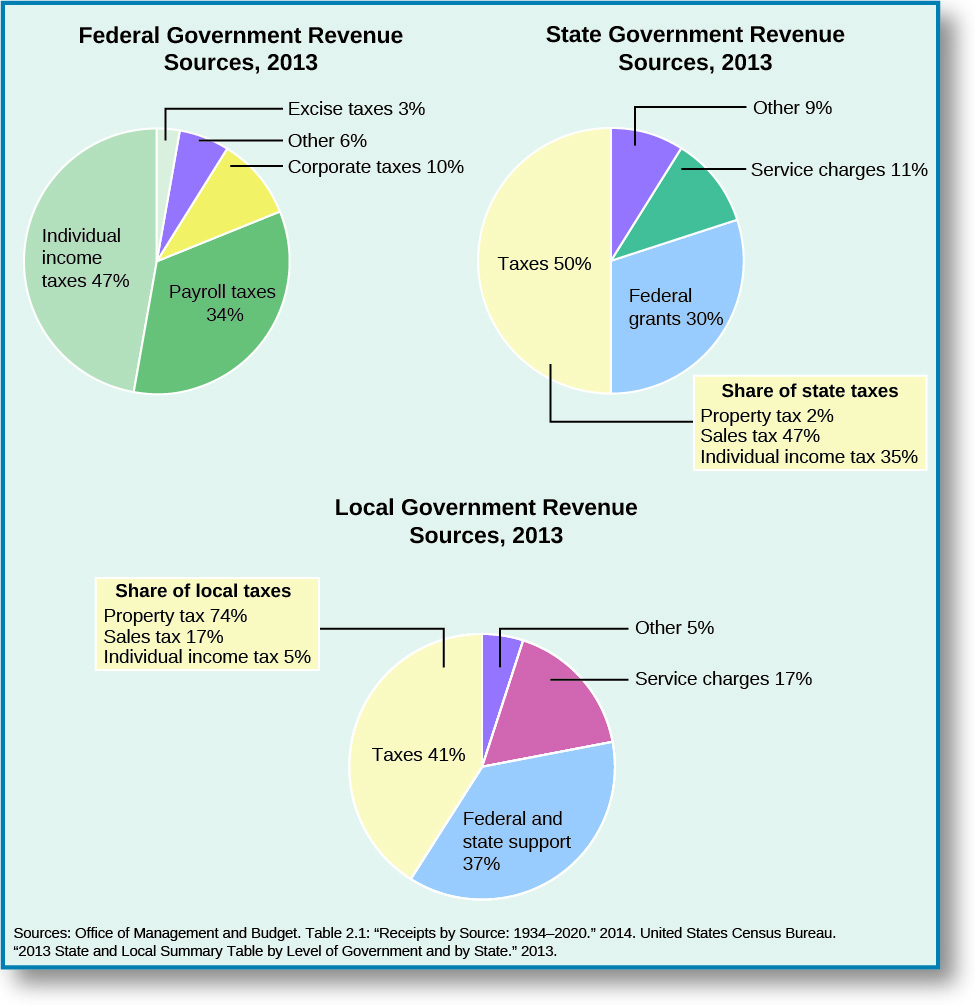

The sources of revenue for federal, state, and local governments are detailed in [link] . Although the data reflect 2013 results, the patterns we see in the figure give us a good idea of how governments have funded their activities in recent years. For the federal government, 47 percent of 2013 revenue came from individual income taxes and 34 percent from payroll taxes, which combine Social Security tax and Medicare tax.

For state governments, 50 percent of revenue came from taxes, while 30 percent consisted of federal grants. Sales tax—which includes taxes on purchased food, clothing, alcohol, amusements, insurance, motor fuels, tobacco products, and public utilities, for example—accounted for about 47 percent of total tax revenue, and individual income taxes represented roughly 35 percent. Revenue from service charges (e.g., tuition revenue from public universities and fees for hospital-related services) accounted for 11 percent.

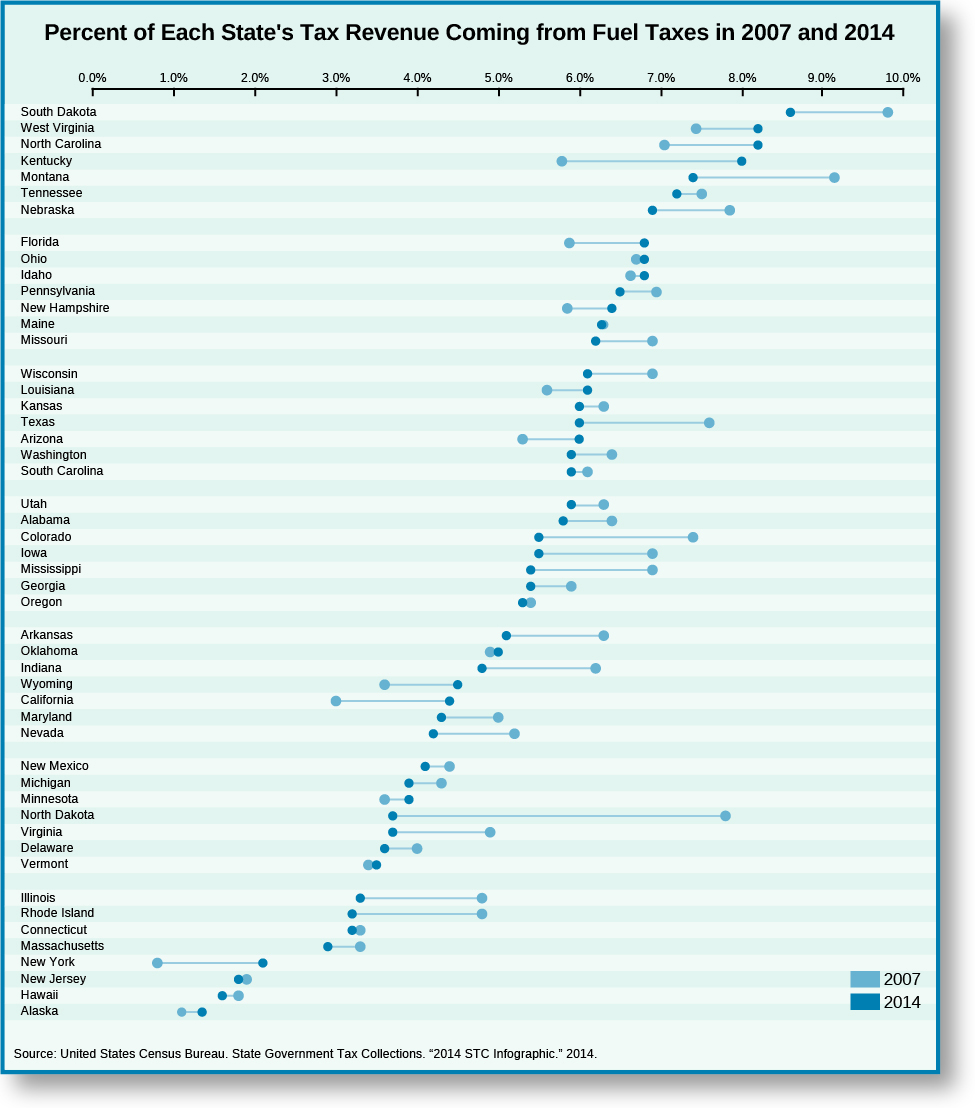

The tax structure of states varies. Alaska, Florida, Nevada, South Dakota, Texas, Washington, and Wyoming do not have individual income taxes. [link] illustrates yet another difference: Fuel tax as a percentage of total tax revenue is much higher in South Dakota and West Virginia than in Alaska and Hawaii. However, most states have done little to prevent the erosion of the fuel tax’s share of their total tax revenue between 2007 and 2014 (notice that for many states the dark blue dots for 2014 are to the left of the light blue numbers for 2007). Fuel tax revenue is typically used to finance state highway transportation projects, although some states do use it to fund non-transportation projects.

The most important sources of revenue for local governments in 2013 were taxes, federal and state grants, and service charges. For local governments the property tax, a levy on residential and commercial real estate, was the most important source of tax revenue, accounting for about 74 percent of the total. Federal and state grants accounted for 37 percent of local government revenue. State grants made up 87 percent of total local grants. Charges for hospital-related services, sewage and solid-waste management, public city university tuition, and airport services are important sources of general revenue for local governments.

Notification Switch

Would you like to follow the 'American government' conversation and receive update notifications?

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|