| << Chapter < Page | Chapter >> Page > |

When accounting transactions are recorded, source documents are used. These documents provide the information necessary to record transactions in the books. They also serve as proof that the transactions did take place.

In the case of cash transactions the following source documents are used:

Cheque book counterfoils when payments are made by cheque.

Receipts when cash is received.

Cash register roll in the case of cash sales.

Cash invoices in the case of cash purchases and cash sales.

Bank deposit slips when cash is deposited into a bank account.

In the case of credit transactions the following source documents are used:

Credit invoices in the case of credit purchases of assets and trading stock, as well as in the case of credit sales of trading stock.

ASSIGNMENT:

Collect examples of the following source documents:

Cheques

Receipts

Invoices

Bank deposit slips

Paste the documents onto A4 sheets of paper and indicate for which type of transaction each document is used. Next to each type of document also indicate the information that appears on that document. Use the completed assignment for your portfolio.

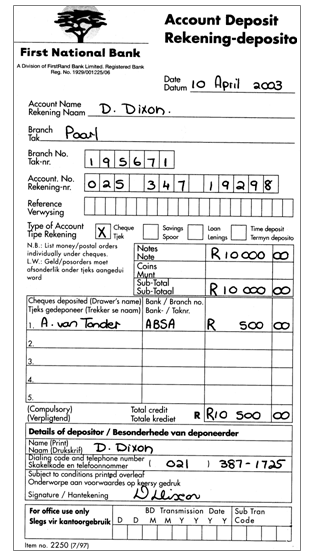

Study the completed deposit slip:

Obtain a blank deposit slip from any bank and complete it by filling in the following information:

Mr P. Tredoux is the owner of PT Services situated at 12 Napier Street, Paarl. On 1 June 2002 he deposits money in the current bank account of the business. The number of this account is 123-456-789.

The deposit is made up as follows:

3 x R50-notes

Nickel to the value of R75.

For control purposes, all cash received in a business is recorded in a journal called the cash receipts journal (CRJ) .

The following are types of transactions involved in the receipt of cash:

1. Cash that the owner of the business deposits in the bussiness’s bank account as his capital contribution.

2. Cash received for services provided.

3. Rental income received for letting a building or part of the building.

When the owner pays capital into the business, he is issued with a receipt. The copy of this receipt is used for the entry in the CRJ.

The following information must be provided on the receipt in order to be able to make an entry in the CRJ:

Date

Receipt number

The owner’s name

The amount paid in

Reason for which the money was paid in

The copy of the bank deposit slip completed to deposit the capital sum directly into the current account of the business, can also be used as a source document.

Study the entry in the CRJ (example 1), which shows how such a transaction is recorded.

On 1 January 2003 the owner, J. Jolie, deposits R50 000 as capital contribution in the bank account of a business called Salon Jolie. (See example 1.)

Notification Switch

Would you like to follow the 'Economic and management sciences grade 8' conversation and receive update notifications?

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|